[ad_1]

When Nvidia announced eye-popping earnings on Wednesday with three-digit year-over-year growth, it was easy to get caught up in the excitement. The company brought in $13.5 billion for the quarter, up 101% over the prior year, and well over its $11 billion guidance.That’s certainly something to get excited about.

Nvidia is benefiting from being a company in the right place at the right time, where its GPU chips are in high demand to run large language models and other AI-fueled workloads. That in turn is driving Nvidia’s astonishing growth this quarter. (It’s worth noting that the company set the groundwork for its current success some time ago.)

“Data center compute revenue nearly tripled year on year, driven primarily by accelerating demand for cloud from cloud service providers and large consumer internet companies for our HGX platform, the engine of generative and large language models,” Colette Kress, Nvidia’s executive vice president and chief financial officer, said in the post-earnings report call with analysts.

This kind of growth brings to mind the heady days of cloud stocks, some of which soared during the pandemic lockdown as companies accelerated their usage of SaaS to keep their workers connected. Zoom, in particular, took off with five quarters of absolutely astonishing growth during that time.

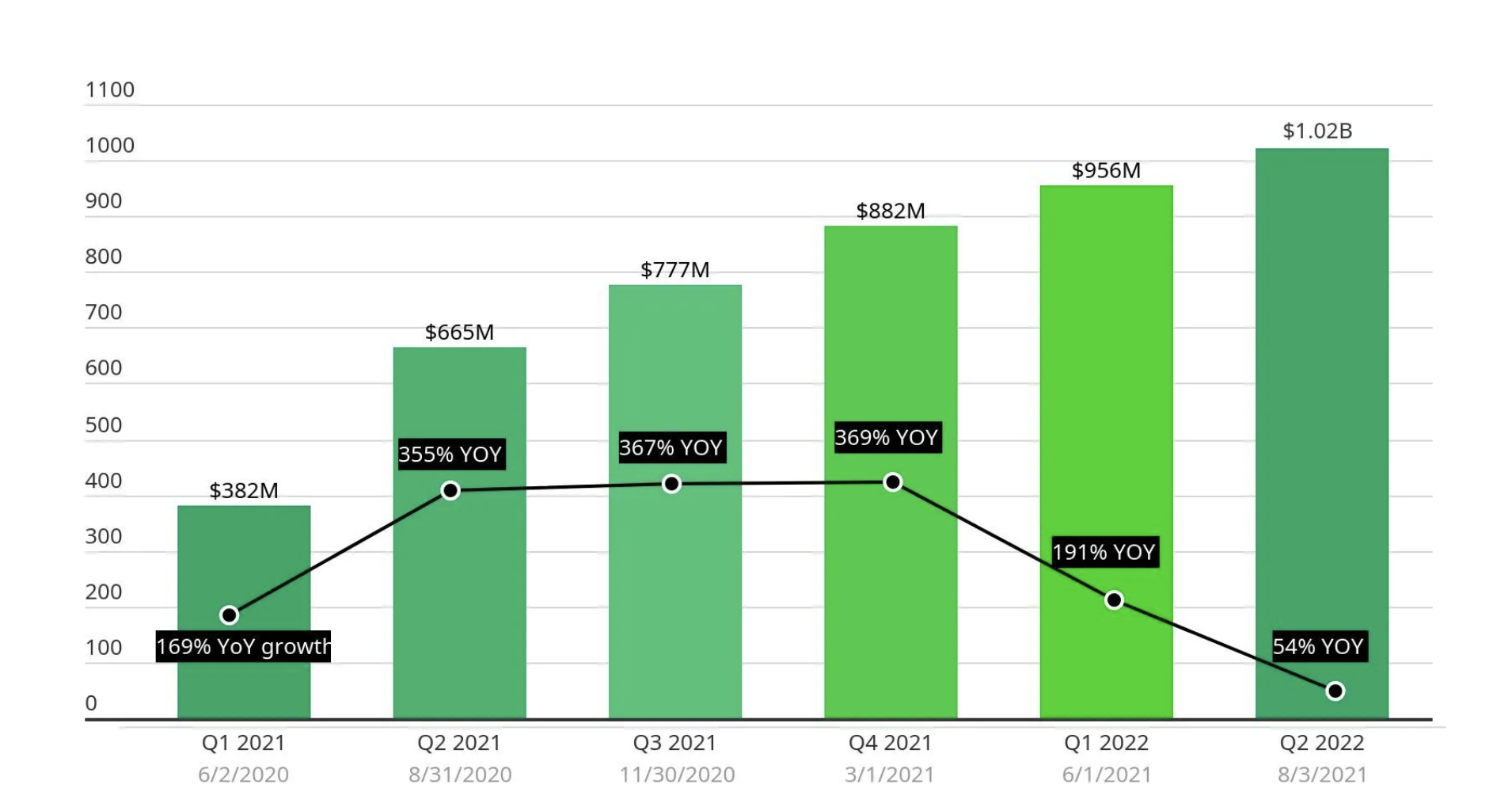

Zoom pandemic fueled growth. Image Credits: TechCrunch

Today, even double-digit growth is long gone. For its most recent report earlier this month, the company reported revenue of $1.138 billion, up 3.6% over the prior year. That follows five straight quarters of single-digit growth, the last three in the low single digits.

Could Zoom possibly be a cautionary tale for a company like Nvidia riding the generative AI wave? And perhaps more importantly, will this drive unreasonable investor expectations about future performance as it did with Zoom?

Data center demand isn’t going anywhere

It’s interesting to note that Nvidia’s biggest growth area is in the data center, and that web scalers are still building at a rapid pace with plans to add over 300 new data centers in the coming years, per a Synergy Research report from March 2022.

“The future looks bright for hyperscale operators, with double-digit annual growth in total revenues supported in large part by cloud revenues that will be growing in the 20-30% per year range. This in turn will drive strong growth in capex generally and in data center spending specifically,” said John Dinsdale, a chief analyst at Synergy Research Group, in a statement about the report.

At least some percentage of this spending will surely be devoted to resources for running AI workloads, and Nvidia should benefit from that, CEO Jensen Huang told analysts on Wednesday. In fact, he believes that his company’s expansive growth is much more than a flash in the pan.

“There’s about $1 trillion worth of data centers, call it, a quarter of trillion dollars of capital spend each year. You’re seeing that data centers around the world are taking that capital spend and focusing it on the two most important trends of computing today: accelerated computing and generative AI,” Huang said. “And so I think this is not a near-term thing. This is a long-term industry transition, and we’re seeing these two platform shifts happening at the same time.”

If he’s right, perhaps the company can sustain this level of growth, but history suggests that what goes up must eventually come down.

Business gravity

If Zoom is any indication, some businesses that see rapid growth for one reason or another can hold onto that revenue in the future. While it’s certainly less exciting for investors that Zoom’s growth rate has sharply moderated in recent quarters, it’s also true that Zoom has continued to grow. That means it has retained all its prior scale and then some.

[ad_2]

Source link